Instant issuance

Instant Issuance offers the best of both worlds, allowing cardholders to have a card in hand and on their phone before leaving the branch. Plus, instant issuance creates higher activation rates and allows cardholders same or next-day spending power.

Additional efficiencies result from offering instant issuance through SaaS (Software as a Service) solutions which provide institutions simplicity and scale, making it a reliable option for those with limited internal IT and other resources. SaaS options are continuing to gain traction, as evidenced by reports that show a growing acceptance of cloud-based solutions by the financial services industry. A 2021 survey of financial service industry executives showed at the time that their firms operated, on average, 38% of their business applications through the cloud, and they anticipated that percentage would increase to 55% in two years. That growing acceptance breeds comfort and familiarity, meaning issuers are increasingly looking to cloud-based solutions as an alternative to hosting an on-site server.

Complementary digital strategy

Complementary digital strategy

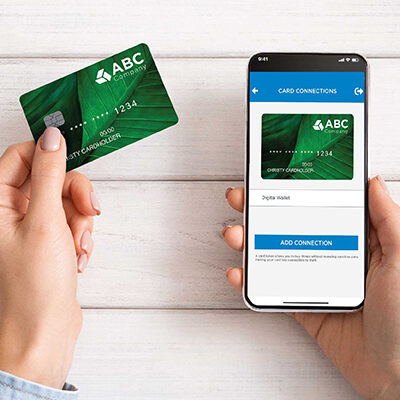

While physical cards remain the most accepted and preferred payment method for purchases, having a card issuance strategy that incorporates a digital component supports cardholder choice and control. So how can financial institutions support their accountholders in adding their physical debit and credit card information to their digital wallets? Digital payment options through push provisioning have allowed card program managers to address the issue more proactively so that users don’t need to figure this out themselves. Push provisioning tokenizes the cardholder’s payment card credentials to a mobile wallet for new or existing accounts, creating a complementary digital option that supports both immediate and ongoing cardholder needs for convenience and choice.